We have the pleasure to announce that we kick off season 3: Digital Cash – Partners and Patents running for the rest of 2021. We aim to do another 36 interviews, focusing on our Digital Cash Partners, our coming patents and any other related subject. All interviews, including season 1 and season 2, are now also available as podcasts.

The final episode in season 2: Cash goes digital – a payment pandemic aired this morning. We want to thank everyone that has been interviewed and all that have followed the interviews. Season 3: Digital Cash – Partners and Patents will start immediately with 36 new episodes that will be released on a more irregular basis during 2021.

All interviews will be available on our website, our YouTube channel, and as podcasts on Spotify, Apple Podcasts and anywhere where podcasts are available, distributed from our new SoundCloud channel. You can subscribe and never miss when we publish new episodes.

Västra Hamnen Corporate Finance AB is the Certified Adviser. Email: ca@vhcorp.se. Telephone +46 40 200 250.

About Crunchfish – crunchfish.com/digitalcash Crunchfish is a tech company with a patent-pending solution for digital offline payments that can be integrated both with the payment rail or in a mobile wallet. The offline solution is globally scalable and makes digital payments more robust as the risks of disruptions and downtime are eliminated. We have also developed Blippit, an app terminal that connects to a cash register system for both online and offline payments. Crunchfish also develops gesture control of smart AR glasses for the consumer market. Crunchfish has been listed on Nasdaq First North Growth Market since 2016 with headquarters in Malmö, Sweden and with representation in India.

Vi har glädjen att meddela att vi startar säsong 3: Digital Cash – Partners and Patents som kommer att sändas under resten av 2021. Vi siktar mot att göra ytterligare 36 intervjuer, med fokus på våra Digital Cash Partners, våra kommande patent och andra relaterade ämnen. Alla intervjuer, inklusive säsong 1 och säsong 2, finns nu även tillgängliga som podcasts.

Det sista avsnittet i säsong 2: Cash goes digital – a payment pandemic sändes i morse. Vi till tacka alla som har intervjuats och alla som har följt intervjuerna. Säsong 3: Digital Cash – Partners and Patents kommer starta omedelbart med 36 nya intervjuer som kommer släppas på mer oregelbunden basis under 2021.

Alla intervjuer kommer finnas tillgängliga på vår hemsida, vår YouTube-kanaloch som podcaster på Spotify, Apple Podcasts och överallt där poddar finns tillgängliga, distribuerade från vår nya SoundCloud-kanal. Du kan prenumerera och aldrig missa när vi släpper nya avsnitt.

För ytterligare information, vänligen kontakta: Joachim Samuelsson, VD för Crunchfish AB +46 708 46 47 88 joachim.samuelsson@crunchfish.com

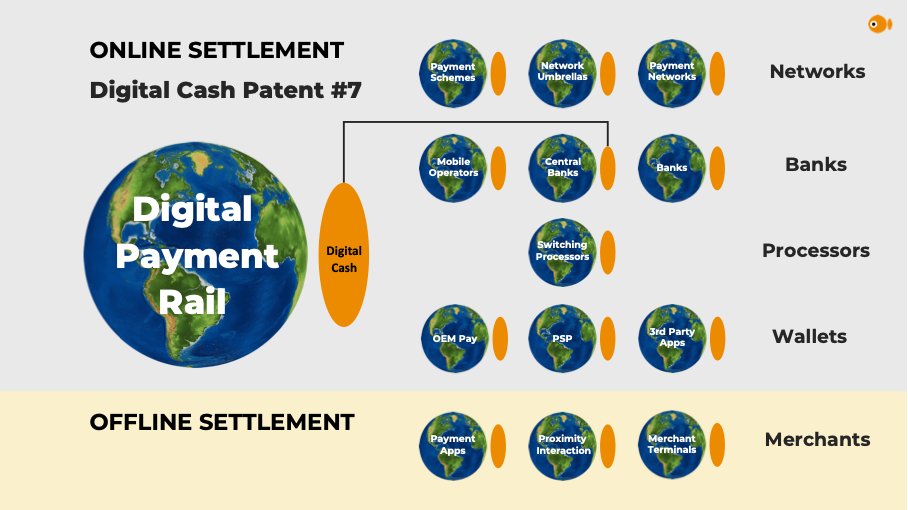

Crunchfish is a technical pioneer within digital payments with its novel Digital Cash solutions that settle physical payments in two steps, first offline and then online, making digital payments robust and also preserves the payer’s integrity. Digital Cash is extremely flexible and interoperable with all types of payment services, even cross-border and cross-schemes. Today Crunchfish announces that its Digital Cash solutions can solve Central Bank Digital Currency, CBDC implementation issues swimmingly easy, without any additional infrastructure. This promises to have a major impact on the whole CBDC industry and accelerate Central Bank implementations.

Crunchfish’s Digital Cash makes it swimmingly easy to implement CBDC, as there is no need for additional infrastructure. Central Banks may just use existing digital payment rails to distribute CBDC. This is a tremendous simplification that will accelerate CBDC roll-outs in the world.

Central Banks in numerous countries are experimenting with Digital Currency using ‘tokenized value instruments’ that represent physical banknotes in digital form. Digital Cash by Crunchfish, on the other hand, use ‘tokenized transaction instruments’ instead, which may be compared to banker’s cheques. Whereas a banknote is a representation of ‘money’, a banker’s cheque represents a ‘money transfer’ between two parties.

Digitizing ‘money transfers’ instead of ‘money’ simplifies CBDC implementations tremendously, as it does not require any additional infrastructure. The ‘tokenized transaction instrument’ approach suggested by Crunchfish as Digital Cash provides all necessary properties of physical cash; robustness, ease of use and preserves the payer’s integrity in relation to banks. To issue its fiat currency, the Central Bank may simply deposit it into a centrally held bank account and invite commercial banks to access and distribute it by means of regular transactions on the existing digital payment rails.

Cash is king of digital payments. It always works, it’s easy to handle and it safeguards personal privacy. Crunchfish preserves these features when cash goes digital. The transformation will be profound as digital cash will be present in all mobile wallets in the future”.

It is worth mentioning that Crunchfish’s flexible Digital Cash solutions with its patent-pending two-tier settlement architecture may be integrated with any payment scheme – Card, Real-Time Payments, Closed-Loop Wallets, Cryptocurrency as well as CBDC. It is therefore certainly still possible to be integrated with any of the current CBDC solutions based on ‘tokenized value instruments’, e.g. Digital Symmetric Cryptography fromCrunchfish’s partner eCurrency or Distributed Ledger Technology blockchains.

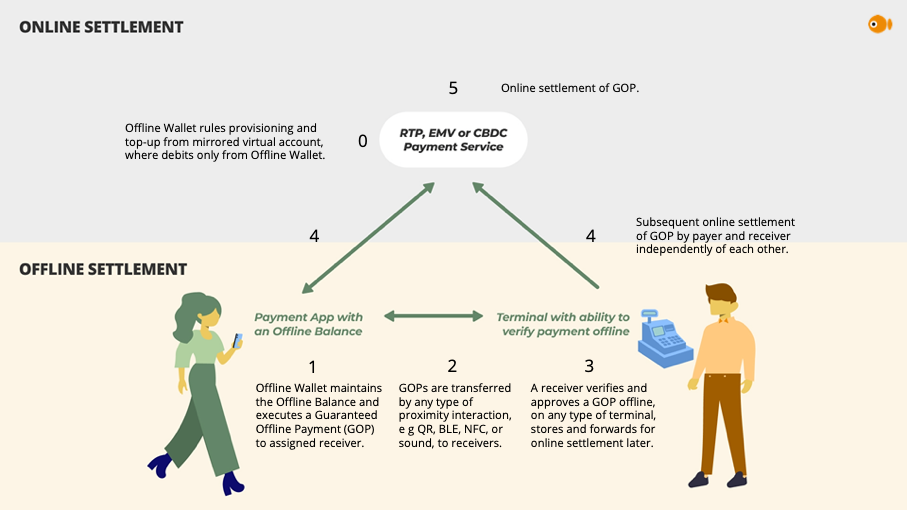

About Digital Cash One year ago, Crunchfish announced offline frictionless mobile payments as a patent pending innovation, making mobile payments services far more robust by introducing the concept of Digital Cash using a two-tier settlement architecture, offline vs. online. The solution leverages the fact that it is not important to the merchants if the transfer to their accounts occurs at the moment-of-payment or a little later, as long as there is trust that the transfer will occur. It is critical however, that the payment experience must be robust, smooth and secure. This implies that the transaction cannot be dependent on the Internet and cloud payment services. No matter how much investments are made into IT-infrastructure, the systems will never be operational 24/7.

The ingenious solution for robust digital payments is based on an implementation of a two-tier settlement architecture. Recently, this approach was proposed by VISA in a research paper describing an Offline Payment System (OPS) protocol applied to CBDC. Crunchfish has alsoenrolled as a VISA Technology Partner.

Crunchfish’s flexible Digital Cash solutions with its patent-pending two-tier settlement architecture may be integrated with any payment scheme – Card, Real-Time Payments, Closed-Loop Wallets, Crypto as well as CBDC.

Crunchfish’s Digital Cash approach is ubiquitous as it may be integrated into any payment scheme and alsoon cards. In addition, Digital Cash is alsopayment services interoperable, cross-borders and cross-schemes, which is key to accelerate CBDC roll-outs and its market acceptance.

Västra Hamnen Corporate Finance AB is the Certified Adviser. Email: ca@vhcorp.se. Telephone +46 40 200 250.

This information is information that Crunchfish AB is obliged to publish in accordance to the EU Market Abuse Regulation. The information was provided by the contact person above for publication on March 2, 2021.

About Crunchfish – crunchfish.com/digitalcash Crunchfish is a tech company with a patent-pending solution for digital offline payments that can be integrated both with the payment rail or in a mobile wallet. The offline solution is globally scalable and makes digital payments more robust as the risks of disruptions and downtime are eliminated. We have also developed Blippit, an app terminal that connects to a cash register system for both online and offline payments. Crunchfish also develops gesture control of smart AR glasses for the consumer market. Crunchfish has been listed on Nasdaq First North Growth Market since 2016 with headquarters in Malmö, Sweden and with representation in India.

Crunchfish är en teknisk pionjär inom digitala betalningar med Digital Cash-lösningar som avvecklar fysiska betalningar i två steg, först offline och sedan online. Det gör digitala betalningar robusta och bevarar även betalarens integritet. Digital Cash är extremt flexibelt och interoperabelt med alla typer av betaltjänster, såväl över landsgränser och från olika betalsystem. Idag meddelar Crunchfish att Digital Cash-lösningar förenklar CBDC-implementation betydligt, eftersom någon ytterligare infrastruktur inte behövs. Detta kommer att ha en stor påverkan på hela CBDC-industrin och accelerera centralbankers implementering av Central Bank Digital Currency, CBDC runtom i världen.

Crunchfishs Digital Cash gör det enkelt att implementera CBDC, eftersom det inte finns något behov av ytterligare infrastruktur. Centralbanker kan använda befintliga digitala betalningsrälsar för att distribuera CBDC. Detta är en enorm förenkling som kommer att påskynda implementeringen av CBDC runtom i världen.

Centralbanker i många länder experimenterar med digital valuta med hjälp av ’tokeniserade värdeinstrument’ som representerar sedlar i digital form. Digital Cash från Crunchfish använder däremot ‘tokeniserade transaktionsinstrument‘ istället, vilket kan jämföras med en postväxel. Medan sedlar representerar anonyma pengar är postväxlar istället penningöverföring mellan två parter.

Att med Digital Cash digitalisera penningöverföring istället för pengar förenklar implementationen av CBDC väsentligt och kräver ingen ny infrastruktur. Digital Cash erbjuder kontanternas egenskaper; robusthet, användarvänlighet och bevarad integritet för betalaren i förhållande till banken. För att ge ut CBDC skapar centralbanken ny valuta genom att deponera den på ett centralbankskonto och därefter bjuda in kommersiella banker till att få tillgång och distribution genom vanliga transaktioner på befintlig digital betalräls.

Cash is king of digital payments. Kontanter fungerar alltid, de är enkla att använda och de skyddar den personliga integriteten. Crunchfish bevarar dessa egenskaper när kontanterna blir digitala. Omvandlingen kommer att bli stor eftersom digitala kontanter kommer att finnas i alla mobila plånböcker i framtiden.

Det är värt att nämna att Crunchfishs flexibla Digital Cash-lösningar med sin patentsökta tvådelade avvecklingsarkitektur kan integreras med alla typer av betalningssystem – kort, realtidsbetalningar, stängda plånböcker, kryptovaluta samt CBDC. Det är därför fortsatt möjligt att integrera Digital Cash med dagens CBDC-lösningar, baserade på ‘tokeniserade värdeinstrument’; t ex Digital Symmetric Cryptography från Crunchfishs partner eCurrency eller blockkedjor baserade på Distributed Ledger Teknologi.

Om Digital Cash För ett år sedan annonserade Crunchfish friktionsfria mobilbetalningar offline som en patentsökt innovation, vilket gjorde mobila betalningstjänster mycket mer robusta genom att introducera konceptet Digital Cash med en tvådelad avvecklingsarkitektur, offline och online. Lösningen bygger på det faktum att det inte är viktigt för handlaren om överföringen till deras konto sker exakt vid betalningstillfället eller lite senare, så länge det finns ett förtroende för att överföringen kommer att ske. Det är dock viktigt att betalningsupplevelsen måste vara robust, smidig och säker. Detta innebär att transaktionen inte kan vara beroende av nätet och molntjänster. Oavsett hur mycket investeringar som görs i IT-infrastruktur kommer nätberoende system aldrig kunna garanteras att alltid fungera.

Den geniala lösningen för robusta digitala betalningar går ut på att implementera en tvådelad avvecklingsarkitektur. Nyligen föreslogs detta tillvägagångssätt av VISA i en forskningsartikel som beskriver ett protokoll för offlinebetalningssystem (OPS) som tillämpas på CBDC. Crunchfish har även antagits som VISA Technology Partner.

Crunchfishs flexibla Digital Cash-lösningar med sin patentsökta tvådelade avvecklingsarkitektur kan integreras med alla betalningssystem – kort, realtidsbetalningar, Closed-Loop Wallets, kryptovalutor såväl som CBDC.

Crunchfishs Digital Cash-lösningar är universellt användbar, eftersom den kan integreras i alla betalningssystem, inklusive på kort. Digital Cash är dessutom interoperabelt mellan olika betaltjänster, över landsgränser och mellan olika betalsystem, vilket är nyckeln till att påskynda utrullning och marknadsacceptans av CBDC.

För ytterligare information, vänligen kontakta: Joachim Samuelsson, VD för Crunchfish AB +46 708 46 47 88 joachim.samuelsson@crunchfish.com

Västra Hamnen Corporate Finance AB är Certified Adviser. Epost: ca@vhcorp.se. Telefon +46 40 200 250.

Denna information är sådan information som Crunchfish AB är skyldigt att offentliggöra enligt EU:s marknadsmissbruksförordning. Informationen lämnades, genom ovanstående kontaktpersons försorg, för offentliggörande den 2 mars 2021.

Crunchfish and Swish today announce that the companies have submitted a joint application to The Swedish Post and Telecom Authority (PTS)’s annual innovation contest, which this year focuses on innovative payment solutions. The goal in the application is to develop a prototype for an offline solution that can be used when net-based payment solutions does not work. The ambition is that the solution will provide the Swedish society with a digital equivalent to cash.

Achieving the vision of an inclusive financial infrastructure requires a complement to today’s network-dependent payment solutions. It is both urgent and critical from a societal point of view for Sweden to modernize cash and make their properties available in digital form. The application to the contest is based on the strength of cash as a robust means of payment, without requirement for network connection or cloud servers and the possibility of maintaining integrity for users.

Crunchfish’s och Swish’s joint application to PTS Innovationaims to make Swish more available, including in contexts in which Swish is not used today, for example when internet connectivity is unavailable. The application is developed in Swish’s test environment based on Crunchfish’s Digital Cash solutions and has similar properties to the e-krona, with the primary difference that the application, in a future potential roll-out, would be issued and guaranteed by the banking system instead of the Swedish Central Bank.

”Swish is an incredible success story for online payments, however Swish demands that the user is online. In the PTS Innovation contest, we are digitalizing cash together with Crunchfish and will show how Swish payments could work in an offline environment”, says Anders Edlund, Head of Business Development at Swish.

”We’re looking forward to build an innovative world-class solution together with Swish, that will contribute to a robust and inclusive digital financial infrastructure in Sweden”, saysJoachim Samuelsson, CEO of Crunchfish.

Background to the contest Since 2010, The Swedish Post and Telecom Authority (PTS) arranges annual innovation contests, contributing to turning smart ideas into reality and improving everyday life. E-commerce and the use of various payment services have increased significantly in recent years, while cash use has fallen sharply. In this development, many people with disabilities – and older people as well – experience difficulties with online shopping, paying bills, using internet banking services and getting started with online identification to identify themselves and approve payments. The gap is widening to those who are comfortable paying digitally. PTS is now looking for innovative and long-term solutions that make it possible for people, regardless of functional ability, to understand and use digital payment services in a simpler and more secure way.

Results in the contest are expected during Q2 2021. More information is available on pts.se/innovation

Om Swish – swish.nu Swish started in 2012 as a cooperation between six of the largest banks in Sweden. Together Danske Bank, Handelsbanken, Länsförsäkringar, Nordea, SEB, Swedbank and Sparbankerna own Getswish AB, the company behind the service. Other banks have since connected to Swish. Today, almost 8 million Swedes has Swish and it has become the most popular means of digital payments among 18-40-year-olds in Sweden.

Västra Hamnen Corporate Finance AB is the Certified Adviser. Email: ca@vhcorp.se. Telephone +46 40 200 250.

This information is information that Crunchfish AB is obliged to publish in accordance to the EU Market Abuse Regulation. The information was provided by the contact person above for publication on March 1, 2021.

About Crunchfish – crunchfish.com/digitalcash Crunchfish is a tech company with a patent-pending solution for digital offline payments that can be integrated both with the payment rail or in a mobile wallet. The offline solution is globally scalable and makes digital payments more robust as the risks of disruptions and downtime are eliminated. We have also developed Blippit, an app terminal that connects to a cash register system for both online and offline payments. Crunchfish also develops gesture control of smart AR glasses for the consumer market. Crunchfish has been listed on Nasdaq First North Growth Market since 2016 with headquarters in Malmö, Sweden and with representation in India.